{kind=link}

Every time you could have cash to put money into equities, a nagging thought inevitably comes up.

“Appears like markets may right from right here. Possibly I ought to wait and make investments after a ten% correction”

Intuitively, ready for a correction looks like a prudent strategy.

However is that this tactic actually as efficient because it feels?

Let’s discover out…

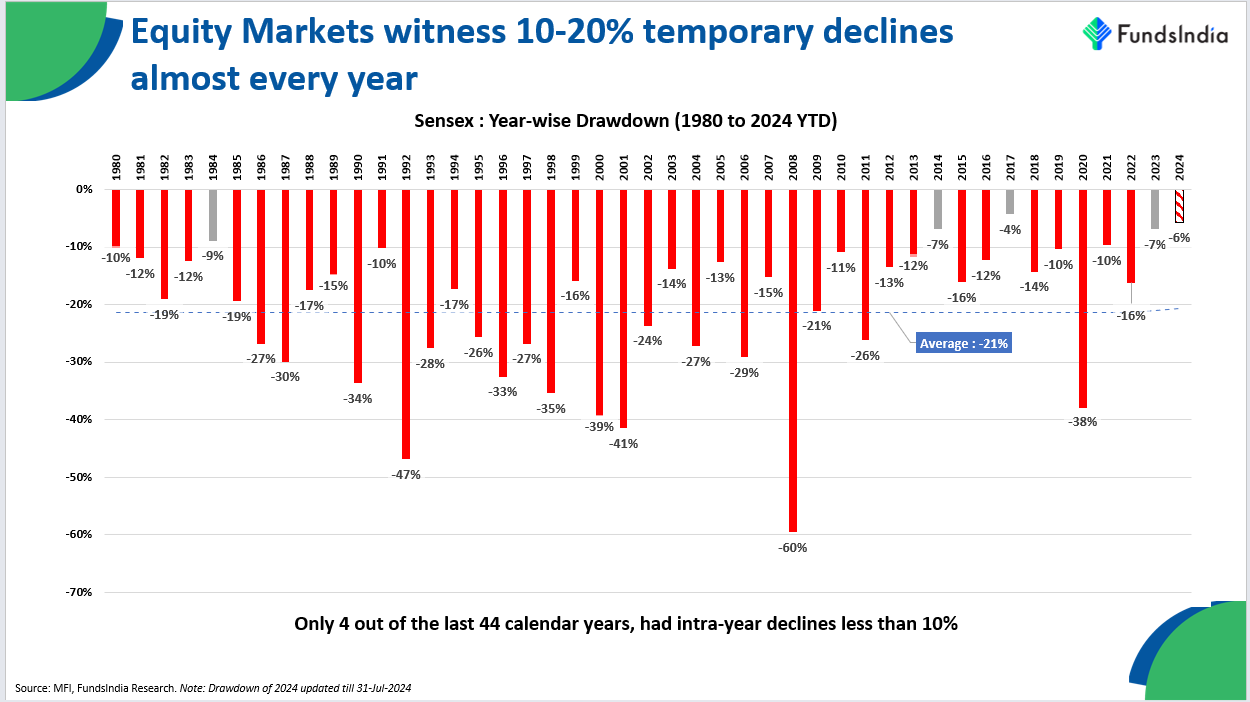

For a greater understanding of market declines, let’s take a look at historical past. Within the under chart, you possibly can see the calendar year-wise drawdowns for Sensex during the last 44+ years.

Yearly noticed a brief market correction. EVERY SINGLE YEAR!

40 out of the 44 years had intra-year declines of greater than 10%!

Takeaway: 10-20% momentary decline yearly is nearly a given!

So, if a 10-20% decline happens virtually yearly then does it not make sense to attend for this decline to take a position new cash?

Easy. Watch for the correction of 10% and make investments the lump sum quantity when it happens.

Seems to be intuitive and logical.

Nonetheless there are 4 challenges {that a} ‘ready for a ten% correction’ technique throws up.

Problem 1: If markets proceed to go up, the correction wanted to re-enter should be a lot bigger than a ten% fall

In case you’re ready to take a position after a ten% correction however the market continues to rally, the pullback required to re-enter will not be simply 10%. You’ll want a bigger correction to take a position once more on the similar ranges.

For instance, in April 2024, when the Sensex was at 75,000, you determined to attend for a ten% correction (all the way down to 67,500) earlier than investing. Nonetheless, previously few months, the market has gone up ~13%, reaching 85,000. Now, you would want a 20% correction to achieve the identical 67,500 stage—excess of the unique 10% you deliberate for.

Briefly, if the market doesn’t right as you anticipate and continues to rise, the drop required to get in at your goal worth turns into considerably larger than 10%.

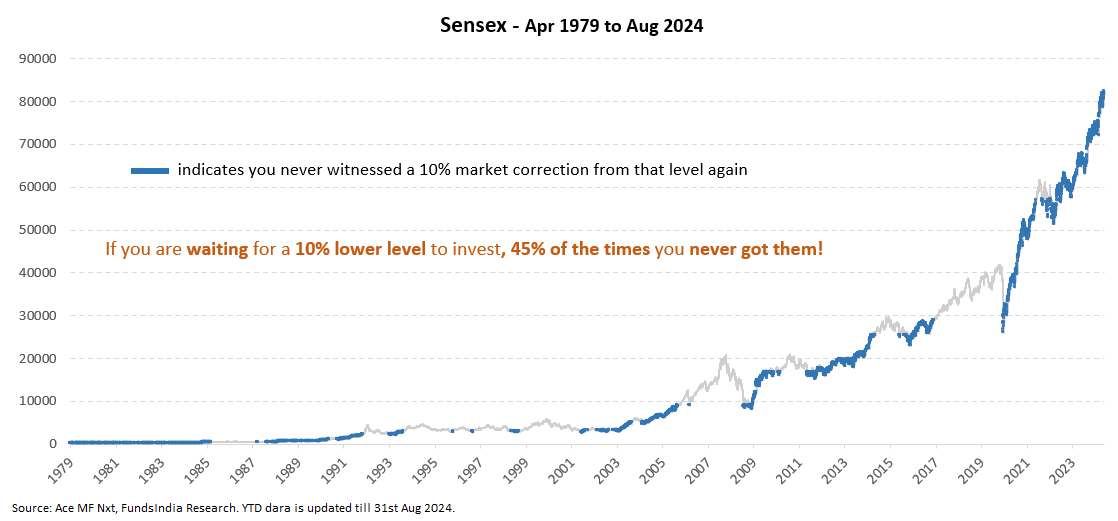

Problem 2: 45% of the occasions you by no means obtained a ten% decrease entry level!

Within the chart under, we’ve analyzed Sensex information from 1979 to the current (Aug-2024), overlaying greater than 45 years. For every day on this interval, we look at the probabilities of the market dropping 10% from that day’s stage for those who determine to attend.

For example, on March 24, 2020, the Sensex was at 26,674. A ten% correction would deliver it all the way down to 24,000. We then test if, between March 25, 2020, and August 31, 2024, the Sensex ever fell under 24,000.

And right here comes the shocker!

45% of the time, the market by no means dropped by 10% from the extent the place you waited.

This might sound to contradict our earlier discovering that 10-20% declines occur virtually yearly.

However right here’s the nuance: whereas these corrections are frequent, they don’t at all times occur instantly. They will happen at any level sooner or later, usually from a lot larger ranges than the place you initially determined to attend.

The difficulty with holding off for a ten% correction is the uncertainty and the massive odds of not getting the required 10% decrease ranges.

Since we don’t know when or at what stage the correction will begin, it’s troublesome to foretell for those who’ll be within the 55% of the time when a ten% drop ultimately happens, or within the 45% of circumstances the place it by no means occurs.

Problem 3: The price of ready will be very excessive for those who get it unsuitable!

From what we’ve mentioned up to now, it’s clear that predicting the precise stage from which market corrections will happen is difficult. However what for those who determine to attend for that correction?

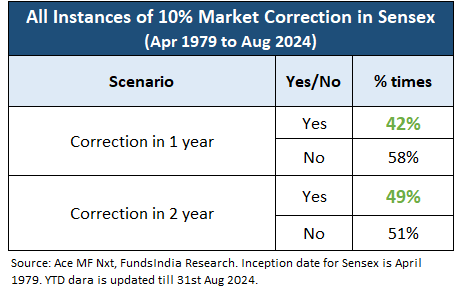

Traditionally, markets expertise a ten% correction about 55% of the time. So, whilst you won’t see a dip as we speak, it may occur subsequent month, or the month after. The query is: how lengthy do you have to wait?

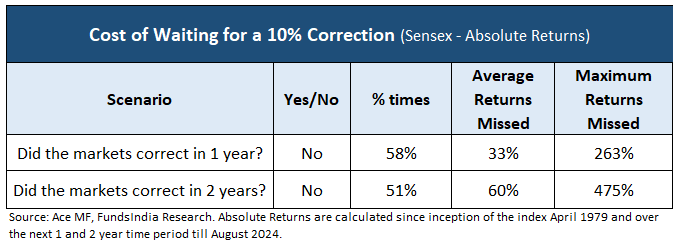

Sometimes, buyers are keen to attend 1-2 years for a correction earlier than they lose persistence and begin reconsidering their technique. Let’s see if ready for this era helps.

Utilizing the Sensex as a reference, we analyzed how usually a ten% correction occurred inside 1-2 years from any given day. For instance, on March 24, 2020, the Sensex stood at 26,674, so we checked whether or not it fell to 24,006 (a ten% drop) throughout the following yr (March 25, 2020 – March 24, 2021) and throughout the subsequent two years (March 25, 2020 – March 24, 2022).

Findings:

- ~50% of the time, the market gave you a ten% correction stage for those who waited 1-2 years.

- In case you consider ready past two years will increase your probabilities, it doesn’t. Since markets solely see a ten% correction 55% of the time in whole, there’s simply a further 5% likelihood it’d occur after two years. However ready that lengthy not often is sensible.

Conclusion:

In case you’re ready for a ten% correction, the technique works greatest inside a 1-2 yr window. Nonetheless, there’s a value to ready.

If the market doesn’t right inside 1-2 years and continues to rally, you miss out on these positive factors. The missed returns compound over time, amplifying the price of staying out of the market.

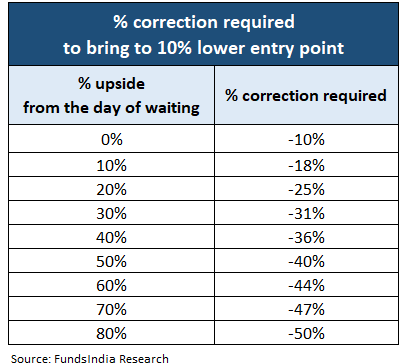

The Value of Ready:

Within the desk under, we calculated the potential returns you miss when the market doesn’t expertise a ten% correction inside 1-2 years:

- On common, you miss out on 33% to 60% upside.

- In excessive circumstances, you would miss a 260% to 475% upside, that means you’ll have missed the chance to multiply your preliminary funding by 3 to six occasions.

Key Takeaway:

Whereas ready for a ten% correction over a 1-2 yr interval can generally work, the price of lacking out on important market rallies will be steep. In some circumstances, the returns foregone by ready may find yourself being far larger than what you’d achieve by catching that correction.

Problem 4 – Behaviorally it’s laborious to enter again at larger ranges

If you’re caught ready for a ten% correction that by no means comes and the market continues to rally, it turns into psychologically difficult to re-enter.

Two key elements make this troublesome:

- Accepting you have been unsuitable: By selecting to take a position at larger ranges after ready for a correction that didn’t occur, you’re primarily admitting that your choice to carry off was incorrect. This admission is psychologically laborious to simply accept, and the discomfort of being “unsuitable” can stop you from re-entering at larger ranges.

- Capturing a everlasting loss: If the market doesn’t right and as a substitute retains going up, you miss out on all of the potential positive factors throughout that point. If you ultimately re-enter at larger ranges, you’ve successfully locked in these missed returns, which turns into a everlasting loss in your portfolio. This missed alternative is usually neglected when calculating total returns.

What do you have to do?

- The dilemma of investing now vs ready for a correction to take a position will come up many occasions all through your funding journey so you will need to settle for this as regular.

- However, ‘ready for a correction’ technique often backfires due to these 4 challenges,

Problem 1 – If markets proceed going up over time, then the required correction to enter again additionally will increase and is way more than only a 10% correction.

Problem 2 – 45% of the occasions you by no means obtained a ten% decrease entry level!

Problem 3 – The price of ready will be very excessive for those who get it unsuitable!

Problem 4 – Behaviorally, it’s laborious to enter again at larger ranges

- To keep away from this psychological urge to preserve ready for a market correction (learn as attempting to time the markets), you will need to have a predetermined rule primarily based framework to deploy lumpsum cash. You’ll be able to select to deploy lumpsum instantly or in case you are valuation aware then you possibly can make investments a portion now and stagger the remaining utilizing a 3-6 months STP.

- At FundsIndia, we comply with a Lumpsum Deployment Framework primarily based on FundsIndia Valuemeter (our in-house valuation indicator). By way of this framework a portion of the lumpsum is straight away invested and the remaining is staggered by way of 3-6 months STP. As a common precept, we deploy quicker when valuations are decrease, and slower when valuations are costly.

Different articles chances are you’ll like

Put up Views:

1,673