{kind=link}

For many of us, saving cash is step one to investing, but 25% to 35% of Individuals reside paycheck to paycheck. This text appears to be like at why persons are residing paycheck to paycheck and the way lower- and middle-income Individuals specifically might be able to improve emergency financial savings resulting in saving extra for retirement. The ideas are simply as related to higher-income individuals as nicely.

Along with volunteering at Habitat For Humanity, I additionally volunteer at an area non-profit group, Neighbor To Neighbor, which affords applications in eviction avoidance, utility shut-off avoidance, reasonably priced housing, housing search, foreclosures prevention, and counseling together with monetary teaching, debt consolidation, and reverse mortgages. Most of the individuals looking for help at Neighbor To Neighbor have skilled an unlucky circumstance equivalent to momentary or everlasting lack of employment, sudden well being problem, divorce, lack of a beloved one, hire inflation, or an accident. My function is to prescreen individuals to get the suitable help inside Neighbor To Neighbor and direct them to exterior sources of help.

As a housing alternative useful resource for Northern Colorado, Neighbor to Neighbor (N2N) companies are designed to fulfill every particular person the place they’re now – from homeless and low-income people looking for a spot to stay; to households needing help to safe their present houses; to potential consumers able to discover the homebuying course of. Our educated housing professionals help shoppers by means of obstacles and develop personalised options to assist them obtain their housing targets.

I hope this text affords some helpful concepts on the way to lower spending and save extra. It’s divided into the next sections:

STEVE BALMER EXPLAINS TODAY’S ECONOMY TO NON-ECONOMISTS

Key Level: The financial system has been stronger than anticipated whereas rates of interest had been rising. It’s an opportune time to get your monetary home so as and save for much less lucky occasions.

Steve Balmer spent 34 years rising Microsoft, 10 years proudly owning the LA Clippers, and began the non-profit USA Details which is rated by Media Bias/Truth Examine as “Least Biased”, “Very Excessive Factual Reporting”, and “Excessive Credibility”. Mr. Balmer supplies this fourteen-minute video, “Is The Financial system Sturdy?” explaining the state of the (2023) financial system in easy phrases. He covers financial progress, inflation (fuel, groceries, hire, housing), employment, earnings, taxes, authorities advantages, demographic shifts, and poverty thresholds.

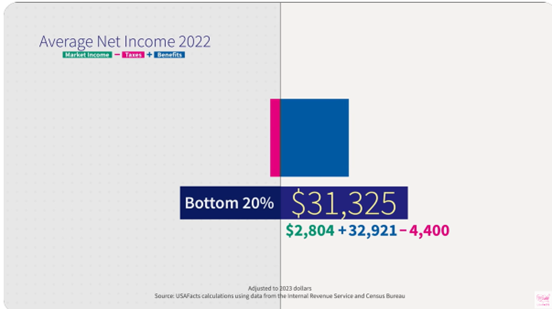

Determine #1 reveals the web earnings of the Backside 20% earnings group which is Market Revenue (Wages, financial savings added to retirement accounts, employer advantages, and earnings from investments) minus taxes (Federal, State, and native) plus authorities advantages (Social Safety, Medicare/Medicaid, meals stamps, tax credit, unemployment advantages…). The online earnings in 2022 of the Backside 20% was $31,325 which was principally authorities advantages, and the web earnings for the Center 20% was $68,575. That was a yr of excessive authorities spending to reduce the impression of the COVID pandemic, and that spending is ending this yr.

Determine #1: 2022 Common Internet Revenue for Backside 20% of Revenue Ranges

Supply: USA Details

Mr. Balmer ended on a constructive word, he continues “to be amazed on the innovation and dynamism of the U.S. financial system and the work ethic of Individuals. The American employee and American financial system ought to by no means ever be underestimated.”

For my part, the rising nationwide debt will most probably end in greater taxes and/or cuts to authorities spending if Congress fails to handle the shortfalls. Social Safety was initially created to fulfill the essential wants of older Individuals for meals and shelter in the course of the Nice Despair. Excessive housing prices and inflation are impacting seniors counting on Social Safety.

FINANCIAL LITERACY: EMERGENCY SAVINGS VERSUS RETIREMENT SAVINGS

Key Level: Folks ought to prioritize constructing emergency financial savings, decreasing debt, after which start to make small contributions to retirement financial savings.

Numerous articles estimate the variety of individuals residing paycheck to paycheck to be between 25% and 75%. From this part, I consider that 25% to 35% of persons are residing paycheck to paycheck and one other 25% to 35% could not have sufficient in financial savings to cowl three months of residing bills. Let’s begin with a definition of residing paycheck to paycheck from Investopedia:

“’Paycheck to paycheck’ is an expression that describes a person who can be unable to fulfill their monetary obligations in the event that they had been unemployed. These residing paycheck to paycheck dedicate their salaries predominantly to bills. The phrase can also imply residing with restricted or no financial savings and check with people who find themselves at higher monetary danger in the event that they had been all of the sudden unemployed or confronted one other monetary emergency.”

Now let’s check out the definition of “emergency financial savings” and “retirement financial savings” from “15+ American Financial savings Statistics to Know in 2024” in FinMasters by David Moadel:

- Emergency financial savings are saved in reserve to fulfill speedy targets or cowl sudden bills or job loss. They’re sometimes saved in financial savings accounts or different accounts that enable quick access.

- Retirement financial savings are supposed to be used after retirement and are normally invested in an IRA, 401(ok), or brokerage account. These financial savings varieties are equally vital, however knowledge on them are collected individually.

General, 22% of households self-reported having no emergency financial savings, and over a 3rd have some financial savings however can not cowl three months of residing bills. Roughly 40% are safer.

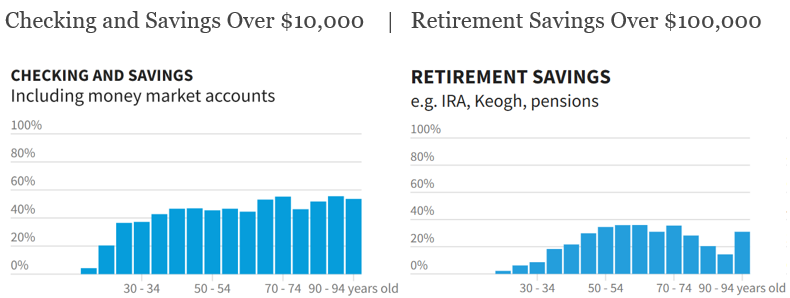

USA Details revealed “Practically half of American households don’t have any retirement financial savings” utilizing the 2022 Survey of Shopper Funds by the Federal Reserve. They’ve interactive charts for Checking/Financial savings, Retirement Financial savings, Monetary Property, and Internet Price. In Determine #2, I present the proportion of individuals by age with at the very least $10,000 of their checking and financial savings accounts together with the proportion of individuals with at the very least $100,000 of their retirement accounts. About 30% to 50% of individuals match into considered one of these classes.

Determine #2: P.c of Folks with Emergency Financial savings Over $10,000, Over $100,00o in Retirement Financial savings by Age

Supply: USA Details

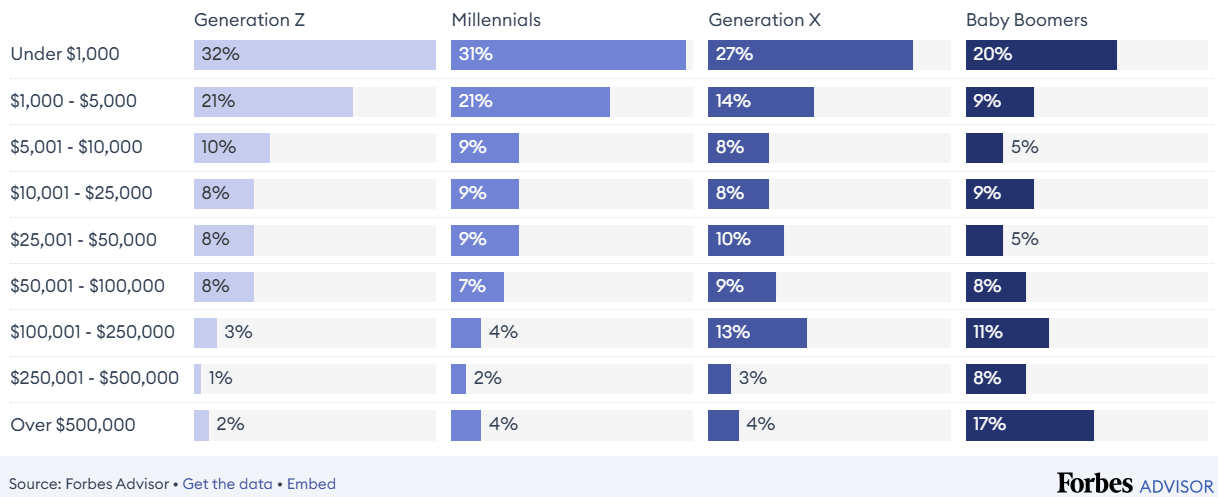

Forbes Advisor’s newest on-line survey of 1 thousand Individuals is summarized by Jamela Adam in “American Financial savings By Technology: How Balances And Targets Fluctuate By Age.” Ms. Adam writes, “In response to our survey, roughly 28% of Individuals throughout all 4 generations at the moment have lower than $1,000 in private financial savings, together with emergency funds, non-workplace retirement accounts, and investments.” Determine #3 accommodates the full financial savings from the survey. Within the occasion of an emergency, respondents mentioned they’d dip into their financial savings (59%), and use debt equivalent to bank cards or loans (30%) whereas others mentioned they’d promote belongings or lower bills (29%).

Determine #3: Complete Financial savings (together with emergency funds, retirement accounts, and investments) by Age Group

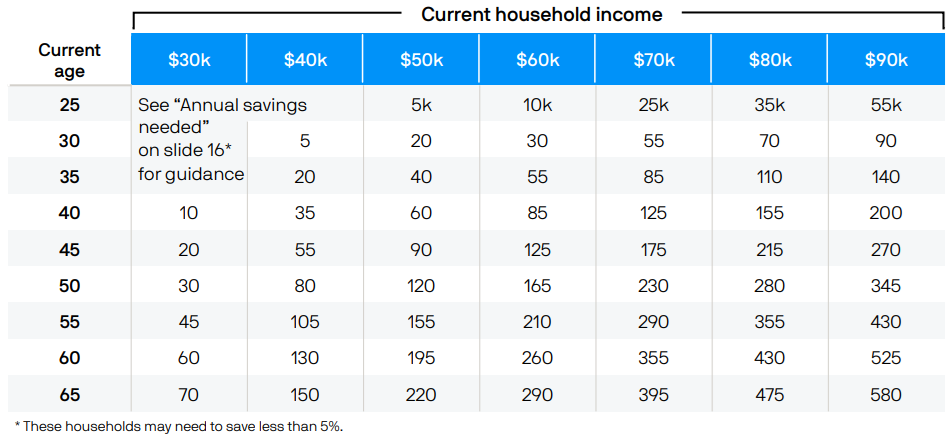

It helps to set targets. JP Morgan’s “2024 Information to Retirement” supplies a helpful desk of checkpoints by age and earnings stage primarily based on an assumed contribution fee of 5% and asset allocation of 60% shares/40% bonds previous to retirement. Most individuals can save greater than the desk beneath by growing their financial savings fee as their earnings rises.

Desk #1: Retirement Financial savings Checkpoints by Revenue and Age

Supply: JP Morgan

AMERICANS’ FINANCIAL STRESS

Key Level: About 25% of Individuals are financially burdened, however some within the lower-middle-income teams could have room to save lots of extra and cut back debt. Having financial savings supplies extra monetary freedom to beat emergencies.

One of many companies that Neighbor To Neighbor affords is “housing search” to assist individuals discover an condominium that they will afford. Many homeless individuals have jobs, however can not afford housing. Some reside paycheck to paycheck and face eviction as a result of they can’t afford the rise in hire.

The US Census Bureau estimates that roughly 37 million individuals (11%) lived in poverty in 2023. Eighteen million (13.5%) had been meals insecure at a while throughout 2023, in accordance with the U.S. Division of Agriculture. Over 21 million renter households spent greater than 30% of their earnings on housing prices in 2023, representing practically half of the renter households in america for whom hire burden is calculated in accordance with the U.S. Census Bureau.

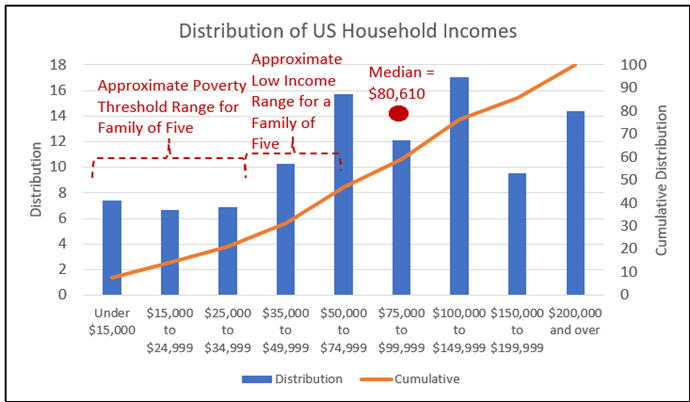

I created the chart beneath from one other US Census Bureau Report, “Revenue in america: 2023”, exhibiting the earnings distribution in 2023. The poverty threshold relies upon upon family measurement. The three lowest earnings ranges in Determine #4 characterize 21% of households. Some individuals will progress from the decrease earnings teams to the upper teams as they acquire expertise, training, and/or expertise. Others could transfer up and down between the degrees primarily based on job stability, job alternatives, well being, or life occasions and preferences.

Determine #4: Distributions of US Family Incomes (2023)

Supply: Writer Utilizing US Census Bureau Report “Revenue in america: 2023”

Gili Malinsky at CNBC explains why persons are residing paycheck to paycheck in “Extra Individuals say they’re residing paycheck to paycheck this yr than in 2023—right here’s why”. The explanations cited are:

- 69% cite inflation

- 59% cite an absence of financial savings

- 28% cite rising rates of interest

- 33% cite bank card debt

- 28% cite medical or healthcare payments

- 21% cite layoffs or lack of earnings

- 15% cite pupil loans

Having bank card debt is each costly and dangerous. Khristopher J. Brooks wrote “Individuals proceed to rack up bank card debt, hitting a file $1.14 trillion” for CBS Information Cash Watch. He described that U.S. customers collectively owe a file $1.14 trillion in bank card debt. He provides, “About 7.18% of cardholders fell into delinquency within the second quarter, up from 5% within the earlier quarter…” Many adults have extra bank card debt than cash saved in emergency financial savings. The common bank card rate of interest is now over 24%.

ASSESSING SPENDING HABITS

Key Level: Having an consciousness of business temptations and the need for monetary independence will help develop higher financial savings habits.

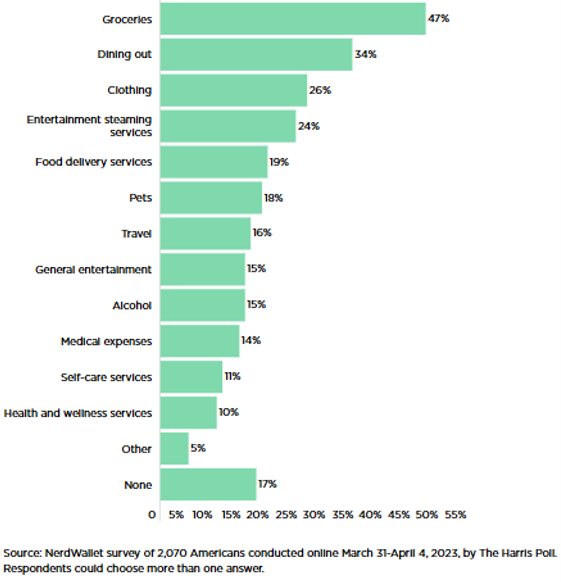

Most individuals have a price range, however individuals usually fail to stay to that price range. Andrew Marder at NerdWallet describes a survey that finds over 80% of Individuals which have a month-to-month price range overspend in “Most Individuals Have a Month-to-month Funds, however Many Nonetheless Overspend”. He provides that near half of Individuals say they need to prioritize emergency financial savings. Determine #5 reveals the classes the place respondents overspend. These classes characterize alternatives for individuals to save cash by adhering to their price range.

Determine #5: Overspending Classes

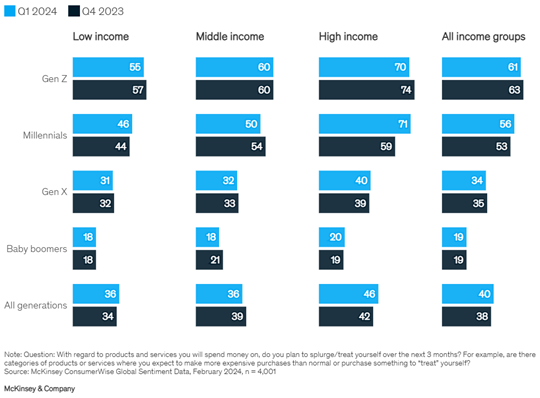

The McKinsey & Firm article, “An replace on US client sentiment: Shopper optimism rebounds—however for the way lengthy?” by Becca Coggins, Christina Adams, Kari Alldredge, and Warren Teichner finds that persons are spending extra on lots of the above classes. Pessimism in regards to the financial system has declined over the previous three years. Over a 3rd of the “respondents say that stabilizing inflation has made them really feel extra optimistic in regards to the financial system”. The factors that I took away are:

- Youthful individuals are inclined to splurge greater than older generations.

- Shoppers indicated they deliberate to extend their spending on most important, semi-discretionary, and discretionary objects over the subsequent three months.

- Seventy-six p.c of customers report buying and selling down—that’s, altering the kind or amount of purchases for higher worth and pricing…

- Shoppers report buying and selling down whereas on the identical time signaling their intent to splurge. Within the third quarter, extra customers throughout earnings and age teams indicated an intent to splurge in contrast with the earlier quarter.

Determine #6: Share of Respondents Meaning to Splurge in 2024, by Demographic, %

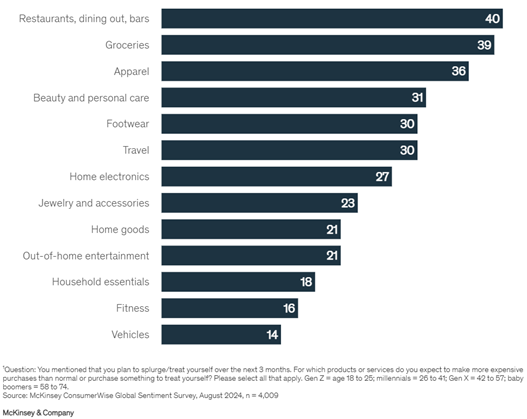

Determine #7: Classes The place Shoppers Intend to Deal with Themselves, % of All Respondents with Intent to Splurge

The above article describes spending growing due to client optimism. Right here is one other article, “Gen Z and millennials are more and more ‘doom spending.’ Right here’s what it’s and the way to cease it” by Sawdah Bhaimiya at CNBC which describes youthful individuals spending extra as a result of they’re pessimistic in regards to the financial system and their future. When some persons are depressed, they have a tendency to spend extra to select themselves up. For example, due to the excessive value of houses, some individuals could quit shopping for a house, and spend the cash as an alternative of saving for a down cost. One resolution Ms. Bhaimiya affords is to extend the “ache of shopping for” equivalent to driving to the shop as an alternative of the benefit of on-line purchasing. Ask your self, “Do I really want this?”

Why are individuals spending extra when many reside paycheck to paycheck or have little financial savings? “Contained in the Psychology of Overspending and How one can Cease” by Jessica Walrack in U.S. Information and World Report describes why some individuals overspend. She lists 5 frequent causes consultants say Individuals are overspending:

- Social Stress: Shopping for what you see others shopping for as a option to sign that you could afford it, too.

- Way of life Creep: When your bills unintentionally creep up as your earnings will increase.

- Emotional Impulse Spending: A research experiences that purchasing enhances emotions of private management, which suggests it’s more likely to alleviate unhappiness.

- Not Accounting for Inflation: In the event you don’t modify your price range to account for price will increase, you’ll possible end up overspending every month.

- Credit score Misconceptions: The reality is that it’s a must to pay again each greenback, plus curiosity and costs.

FINANCIAL COUNSELING VERSUS FINANCIAL ADVISORS

Key Level: Monetary Counselors can help in enhancing monetary literacy and finish residing paycheck to paycheck if an individual is prepared to keep it up.

Monetary advisors normally assist to find out investments, asset location, and asset allocation, and produce a monetary plan. Monetary counselors present a unique service. Folks residing paycheck to paycheck usually have low financial savings so a monetary counselor will in all probability be of extra profit than a monetary advisor. John Egan describes the companies and accreditation of a monetary counselor in addition to the place to find one in “What Is A Monetary Counselor?” for Forbes Advisor.

Jean Folger supplies a “Information to Hiring a Monetary Counselor“ in Investopedia. She lists typical assist and steering offered as:

- Construct financial savings

- Create (and follow) a price range

- Create a plan to pay down debt

- Take care of a right away monetary disaster

- Decide when you’re eligible for tax credit

- Enhance your credit score rating

- Handle traces of credit score

- Handle pupil loans

- Modify ineffective cash habits

- Navigate obtainable public advantages and neighborhood sources

- Set and notice monetary targets

- Perceive primary monetary rules

- Enhance your total monetary well being

- Refer you to an funding advisor or monetary planner if you’re prepared

- Some monetary counselors have further coaching in different areas

Ms. Folger says that the value charged by a monetary counselor is normally decrease than when working with a monetary advisor or licensed monetary planner. “Monetary counselors who work in personal apply could provide a free preliminary session after which cost a flat price for any subsequent conferences. Others could cost an hourly fee or a month-to-month subscription,” she provides.

IMPROVING SAVING HABITS

Key Level: Create a price range. Minimize out pointless subscriptions and companies. Automate your financial savings. Repay costly debt or consolidate it with a decrease rate of interest. Simply say “no” to these impulse purchases. Go for a stroll within the park as an alternative of strolling by means of the mall. Take into account a go to to a Monetary Counselor.

Emily Batdorf wrote “Residing Paycheck To Paycheck Statistics 2024” in Forbes Advisor, a “2023 survey performed by Payroll.org.” When requested how individuals residing paycheck to paycheck plan to save cash, respondents cited three main methods.

- Practically 63% of respondents say making meals at house and packing meals when going out is their main approach of saving cash.

- The second most typical option to save was reducing again on nonessential bills (57%).

- The third is purchasing secondhand (50%).

Non-profit organizations like Habitat For Humanity, Goodwill, Salvation Military, and The Arc elevate cash by means of donations to their second-hand shops. There are a lot of bargains. If you wish to downsize or clear out your attic think about donating to a worthy group.

To cease residing paycheck to paycheck by yourself, Julia Kagan suggests in “Residing Paycheck to Paycheck: Definition, Statistics, How one can Cease” at Investopedia that you could:

- Assessment your price range. Budgeting depends on monitoring your bills towards your earnings… Take a look at each greenback you spend over a month to see if you will discover out what could have elevated your spending.

- Be sure you are saving. Residing paycheck to paycheck usually precludes saving. If in case you have little to no financial savings, begin small—put aside 1% of every paycheck ($10 for each $1,000 you earn). And automate it so that you just aren’t tempted to spend it.

- Repay your debt. One draw back of getting no monetary cushion is counting on bank cards with excessive APRs to cowl emergencies of various sizes. Relying in your scenario, there are quite a few methods to pay down bank card debt, together with utilizing a debt snowball technique to repay the smallest debt first, utilizing a steadiness switch on a bank card with 0% curiosity for a yr or extra, or getting a private mortgage or a debt consolidation mortgage.

- Improve your earnings. Whether or not which means beginning a aspect hustle, asking for a elevate or a promotion, or discovering a better-paying job, the additional money will help you begin setting apart extra financial savings and/or paying off your debt quicker.

Take into account a non-profit monetary counselor just like the Nationwide Basis for Credit score Counseling (NFCC) which was based in 1951 and works with customers by means of one-on-one monetary evaluations. The press launch, Nationwide Basis for Credit score Counseling Warns of Skyrocketing Shopper Monetary Stress, describes a “vital stage of monetary pressure the place households are reducing again on meals bills and private financial savings”.

Neighbor To Neighbor’s (the place I volunteer) Monetary Teaching contains 1) Private Credit score Rating Evaluation & Mortgage Choices, 2) Customized Budgeting Plan, and three) Referrals for lenders, brokers & different housing professionals. As a part of the teaching, the supervisor helps shoppers analyze their spending habits to know the place they’re spending their cash.

Roughly two-thirds of employers provide 401(ok) financial savings. Elizabeth Gravier says in an article at CNBC, “A 401(ok) match is like free cash — right here’s the way it works” that “98% of firms that provided a 401(ok) in 2023 matched their workers’ contributions to some extent”. The standard match is 3 to five%. That is a further incentive to save lots of at the very least the minimal quantity to get the employer-matching contribution. If an worker contributes 5% and the employer contributes 3% then the financial savings fee is 8%.

For individuals with low and reasonable incomes, the Retirement Financial savings Contributions Credit score, also referred to as the Saver’s Credit score, permits an individual “to take a tax credit score for making eligible contributions to your IRA or employer-sponsored retirement plan”. The utmost contribution quantity is $2,000 ($4,000 if married submitting collectively), making the utmost credit score $1,000 ($2,000 if married submitting collectively).

Closing

I consider within the “Pay your self first” philosophy the place you get monetary savings as a precedence earlier than you spend it. I additionally consider in sustaining emergency financial savings as a precedence earlier than investing. Life can have its challenges and emergency financial savings would be the distinction between monetary hardship and touchdown in your toes. If an individual resides paycheck to paycheck then it might be worthwhile to go to a Monetary Counselor/Coach.